Here’s the latest Business View column from James Penn of Capital International.

With recent scenes in the House of Commons looking like something out of Venezuela, we at Capital International have updated our forecasts once again to reflect the current political volatility in the United Kingdom.

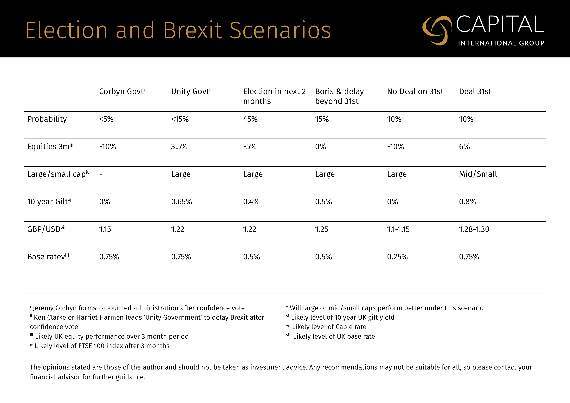

We attach above the same slide we included in this newspaper earlier in the month, but have adjusted the accompanying probabilities to reflect our thoughts on changes in likely outcomes.

The likelihood of an election in the next couple of months has grown significantly to 45% under our reckoning. Clearly the minority Conservative government wants one – the opposition have yet to comply though, and the government has as yet come nowhere near to getting the required number of votes to dissolve Parliament under the Fixed Term Parliament Act.

-(1).jpeg?width=209&height=140&crop=209:145,smart&quality=75)

Tempers are heated, opinions are boiling over, agreement and consensus are short on the ground, but there is at present no sign of any means of resolving this impasse.

Meanwhile, we believe that the chances of No Deal and an agreed Deal have dropped to about 10% each. No Deal seems to have been ruled out by recent legislation, while getting agreement on a deal (given the previous one was voted down three times) looks almost impossible in the current fractious atmosphere. The possibility of a ‘Unity Government’, led by someone like Ken Clarke or Harriet Harman, entrusted with the task of carrying the country through the October 31 deadline and asking the EU for an extension (on the basis that Boris refuses to ask for it), has increased in our estimation – perhaps to 15%. Would a ‘Unity Government’ agree to an election as soon as the extension was granted, or would it plough on for the remaining two and a half years of the current Parliamentary term… Who knows?

While Boris has claimed he would rather be ‘dead in a ditch’ than seek an extension, the most likely outcome surely is Boris asking for the extension and then immediately (on October 19) calling for an election.

By then there will be no excuse for the opposition declining one or prevaricating. It would seem probable to us that Parliament agrees to one on the basis that politics is currently log-jammed, and it is simply impossible for any party in this environment to get its domestic agenda through.

How that election goes is anyone’s guess. The Tories will fight on a Brexit ticket, and will probably gain some Labour seats in the North and the Midlands, but will likely lose seats in the South to the Liberals, and in Scotland to the SNP.

Some polls have forecast the Conservatives getting a 100-plus majority with only 30% of the votes, with the opposition split, but the polls showed similar outcomes for Mrs May ahead of the 2017 election and we all know how accurate they were. The Tories may have to deselect some of the 21 ‘rebels’ who had the whip taken away from them in September over the so-called Benn bill (which forced an extension on the government), and there is a danger that this could alienate some previously loyal Conservative voters.

Over on the other side of the Atlantic the political situation looks similarly precarious – with President Trump once again looking in danger of being impeached over the July conversation he had with the president of Ukraine, and with claims of a Whitehouse cover up over this phone call given the comments made about Democratic Presidential candidate Joe Biden’s son. And this comes only a matter of months after Trump had been given the carte blanche over a previous attempt to impeach him (in relation to tampering by foreign powers in the 2016 Presidential election).

Trump may be able to brush this one off like he has done before. On the other hand, the scandal may fester away for months with damaging consequences for the President, in rather the same manner that the Watergate scandal undermined President Nixon, eventually making his position untenable. This would not be good for stock markets, given the President’s pro-business policies and tax cuts have been a major factor in the ‘Trump Bump’ and the strong rally in equities we have seen since 2016.

Overall, the political situation still looks precarious in most places. Markets have rallied into the quarter end, with a good month in September.

But it remains very difficult to see where they go from here over the remainder of the year, and there could be further volatility ahead yet. We are roughly at the point in the year (early October 2018) when stocks began falling in their calamitous final quarter at the end of last year. Things rarely replicate themselves in exactly the same way and, hopefully, there won’t be a repeat of that this time, but in the current environment one can never be certain.

The opinions stated are those of the author and should not be taken as investment advice. Any recommendations may not be suitable for all, so please contact your financial adviser for further guidance. The value of investments can go down as well as up.

Comments

This article has no comments yet. Be the first to leave a comment.